%matplotlib inline

from sklearn.model_selection import KFold, StratifiedKFold

import numpy as np

import pandas as pd

import lightgbm as lgb

from sklearn.metrics import roc_auc_score

from lightgbm import LGBMClassifier

from lightgbm import cv

import gc

import random

import matplotlib.pyplot as plt

### What happens when you don't implement any predictions, but instead focus on non-linear interactions as your..

### ..core form of analysis

## Machine Learning Benchmarks

## In linear models a PCA step can work nicely

from sklearn.model_selection import cross_val_score, GridSearchCV, KFold

from sklearn.linear_model import LinearRegression

from sklearn.linear_model import Ridge

from sklearn.linear_model import Lasso

from sklearn.ensemble import RandomForestRegressor, GradientBoostingRegressor, ExtraTreesRegressor

from sklearn.svm import SVR, LinearSVR

from sklearn.linear_model import ElasticNet, SGDRegressor, BayesianRidge

from sklearn.kernel_ridge import KernelRidge

from xgboost import XGBRegressor

from sklearn.linear_model import Ridge, RidgeCV, ElasticNet, LassoCV, LassoLarsCV

## Structure Routine Loading and Holdout

df = pd.read_excel("data/Satisfaction Survey.xlsx")

pickle.dump(df, open("data/df_airline.p", "wb"))

### to load holdout for preprocessing to be the same as model processing dataframe

### df = pickle.load(open("holdout_airline.p", "rb"))

### Some regression problems have a low cardinality and seems like it might be easier to represent as a

### classification problem, instead, I will stick with the regression narrative.

### I am sure price sensitivity is a self reported measure as it is a survey.

What predictor variables shows the strongest power in predicting:

- Departure Delays

- Arrival Delays

- Cancelations

- Satisfaction

Of course the majority of these prediction tasks are constrained by the data available, ..

the only true prediction excercise is predicting customer satisfaction.

pd.options.display.max_columns = None

df.head()

| Satisfaction | Airline Status | Age | Age Range | Gender | Price Sensitivity | Year of First Flight | No of Flights p.a. | No of Flights p.a. grouped | % of Flight with other Airlines | Type of Travel | No. of other Loyalty Cards | Shopping Amount at Airport | Eating and Drinking at Airport | Class | Day of Month | Flight date | Airline Code | Airline Name | Orgin City | Origin State | Destination City | Destination State | Scheduled Departure Hour | Departure Delay in Minutes | Arrival Delay in Minutes | Flight cancelled | Flight time in minutes | Flight Distance | Arrival Delay greater 5 Mins | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 3.5 | Gold | 35 | 30-39 | Male | 1 | 2011 | 14.923291 | 11 to 20 | 5 | Business travel | 0 | 0 | 60 | Eco | 6 | 2014-03-06 | MQ | EnjoyFlying Air Services | Madison, WI | Wisconsin | Dallas/Fort Worth, TX | Texas | 6 | 0.0 | 0.0 | No | 119.0 | 821 | no |

| 1 | 5 | Platinum | 46 | 40-49 | Female | 1 | 2012 | 28.800558 | 21 to 30 | 24 | Business travel | 1 | 0 | 75 | Eco | 15 | 2014-01-15 | MQ | EnjoyFlying Air Services | Milwaukee, WI | Wisconsin | Dallas/Fort Worth, TX | Texas | 10 | 13.0 | 0.0 | No | 114.0 | 853 | no |

| 2 | 2 | Blue | 62 | 60-69 | Male | 1 | 2005 | 63.807531 | 61 to 70 | 8 | Personal Travel | 0 | 0 | 30 | Eco | 24 | 2014-01-24 | MQ | EnjoyFlying Air Services | Milwaukee, WI | Wisconsin | Dallas/Fort Worth, TX | Texas | 12 | 0.0 | 0.0 | No | 122.0 | 853 | no |

| 3 | 1 | Blue | 67 | 60-69 | Female | 1 | 2010 | 41.841004 | 41 to 50 | 5 | Personal Travel | 0 | 0 | 60 | Eco | 6 | 2014-03-06 | MQ | EnjoyFlying Air Services | Milwaukee, WI | Wisconsin | Dallas/Fort Worth, TX | Texas | 9 | 12.0 | 1.0 | No | 127.0 | 853 | no |

| 4 | 4 | Blue | 44 | 40-49 | Female | 1 | 2003 | 12.552301 | 11 to 20 | 1 | Business travel | 0 | 0 | 90 | Business | 20 | 2014-03-20 | MQ | EnjoyFlying Air Services | Madison, WI | Wisconsin | Chicago, IL | Illinois | 9 | 6.0 | 24.0 | No | 30.0 | 108 | yes |

# Fits should happen on the train and be applied on test and train

df = pickle.load(open("data/df_airline.p", "rb"))

np.random.seed(10)

df.loc[38897,"Satisfaction"] = 4

df.loc[38898,"Satisfaction"] = 4

df.loc[38899,"Satisfaction"] = 4

df["Satisfaction"] = pd.to_numeric(df["Satisfaction"])

import numpy as np

#Keeping 15% for the validation set, thats about 1000 instances to test on

from sklearn import preprocessing

le = preprocessing.LabelEncoder()

for col in df:

if df[col].dtype == 'object':

df[col] = le.fit_transform(df[col])

msk = np.random.rand(len(df)) < 0.30

df["is_test"] = msk

X_train = df[df["is_test"]==False].drop(col_drop,axis=1)

y_train = df[df["is_test"]==False]["Satisfaction"]

test_df = df.loc[df.is_test, :]

msk = np.random.rand(len(test_df)) < 0.50

test_df["is_holdout"] = msk

holdout = test_df[test_df["is_holdout"]==True].reset_index(drop=True).drop("is_holdout",axis=1)

test_df = test_df[test_df["is_holdout"]==False].reset_index(drop=True).drop("is_holdout",axis=1)

X_test = test_df.drop(col_drop, axis=1)

y_test = test_df["Satisfaction"]

X_hold = holdout.drop(col_drop, axis=1)

y_hold = holdout["Satisfaction"]

del holdout

X_full = pd.concat((df[df["is_test"]==False], test_df),axis=0).drop(col_drop, axis=1)

y_full = pd.concat((df[df["is_test"]==False], test_df),axis=0)["Satisfaction"]

d_train = lgb.Dataset(X_train, label=y_train)

d_test = lgb.Dataset(X_test, label=y_test)

d_hold = lgb.Dataset(X_hold, label=y_hold)

#d_test = lgb.Dataset(X_test, label=y_test.sample(len(y_test)).reset_index(drop=True)) ## quick bench

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/ipykernel/__main__.py:7: SettingWithCopyWarning:

A value is trying to be set on a copy of a slice from a DataFrame.

Try using .loc[row_indexer,col_indexer] = value instead

See the caveats in the documentation: http://pandas.pydata.org/pandas-docs/stable/indexing.html#indexing-view-versus-copy

y_full.shape

(110343,)

X_full.shape

(110343, 29)

### I doubt these parameters can be improved further - the gap between training and valid has decreased.

### learning curves should not be used to jusde variance and bias - instead to see if more data will help.

params = {

'boosting_type': 'gbdt',

'objective': 'regression',

'metric': 'mae',

'subsample':.80,

'num_leaves':50,

"seed":10,

'min_data_in_leaf':180,

'feature_fraction':.80,

"max_bin":100,

'max_depth': 6,

'learning_rate': 0.1,

'verbose': 0, }

Fast CV

## Best Score

## Only difference is - this is quick and dirty (Rapid Testing)

## There is a gap between validation and training, so it is overfitting

## Automated is not necessary if you know your parameters - too much of a hastle

## Do anything you can to improve validtion score

## Remember CV is only there for parameter optimisation and that is what you are using it for.

## This is just normal validation and not folder validation

model = lgb.train(params,d_train, num_boost_round=10000,valid_sets=[d_train, d_test], early_stopping_rounds=103,verbose_eval=100,)

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

Training until validation scores don't improve for 103 rounds.

[100] training's l1: 0.505691 valid_1's l1: 0.51388

Early stopping, best iteration is:

[78] training's l1: 0.507267 valid_1's l1: 0.513656

Medium CV

## Medium Score

## Only difference is - this takes longer but more accurate (Medium Testing)

## Holdout set is (long form testing)

from lightgbm import cv

from lightgbm import Dataset

## Here you don't have to provide a validation set as it will cross validae

def get_score(X, y, usecols, params,seeder,depther, verbose =20):

dtrain = Dataset(X[usecols], y)

# params["max_depth"] = depther

eval = cv(params,

dtrain,

nfold=3,

num_boost_round=20000,

early_stopping_rounds=160, ## After it stopped how long should go on.

verbose_eval=verbose,

stratified=False, ## by default it is true, so have to set to false

#verbose_eval=-1,

seed = seeder,

show_stdv=True)

#print(eval)

return eval, min(eval['l1-mean']), eval["l1-mean"].index(min(eval["l1-mean"]))

eval, score, seed_best = get_score(X_full,y_full ,list(X_full.columns), params, seeder=10,depther=6)

print("score: ", score)

[20] cv_agg's l1: 0.531576 + 0.00124649

[40] cv_agg's l1: 0.51668 + 0.00128588

[60] cv_agg's l1: 0.5159 + 0.00137973

[80] cv_agg's l1: 0.516048 + 0.00141066

[100] cv_agg's l1: 0.516196 + 0.00134864

[120] cv_agg's l1: 0.516425 + 0.00133711

[140] cv_agg's l1: 0.516672 + 0.00123967

[160] cv_agg's l1: 0.516859 + 0.00126381

[180] cv_agg's l1: 0.517057 + 0.00117263

[200] cv_agg's l1: 0.517354 + 0.00125141

[220] cv_agg's l1: 0.517525 + 0.00128193

score: 0.5158844396077821

Ensemble CV

## Worst Score

## This is a submission CV to identify iterations for the different parameter elections of chosen

## ensemble models.

random_seeds = [5, 1, 9 ,12, 20]

depths = [6,6,6,6,6]

seed_dict = {}

final_score = 0

for seedling, deepling in zip(random_seeds,depths ): ## Here is where you add parameter adaptions

eval, score, seed_best = get_score(X_full,y_full ,list(X_full.columns), params, seeder=seedling,depther=deepling, verbose=-20)

final_score += score

seed_dict[seedling] = seed_best

print("score: ", final_score/5)

score: 0.5160619578901716

Fast Submission

y_pred = model.predict(X_hold)

from sklearn.metrics import mean_absolute_error

mean_absolute_error(y_hold, y_pred)

0.5135152460923419

n_splits = 5

cvv = KFold(n_splits=n_splits, random_state=42)

oof_preds = np.zeros(X_full.shape[0])

sub = y_hold.to_frame()

sub["Target"] = 0

from sklearn.metrics import mean_absolute_error

feature_importances = pd.DataFrame()

avg_iter = 0

for i, (fit_idx, val_idx) in enumerate(cvv.split(X_full, y_full)):

X_fit = X_full.iloc[fit_idx]

y_fit = y_full.iloc[fit_idx]

X_val = X_full.iloc[val_idx]

y_val = y_full.iloc[val_idx]

print(X_full.shape)

print(X_fit.shape)

model = LGBMRegressor(

**params

)

model.fit(

X_fit,

y_fit,

eval_set=[(X_fit, y_fit), (X_val, y_val)],

eval_names=('fit', 'val'),

eval_metric='mae',

early_stopping_rounds=150,

verbose=False

)

print("itteration: ", model.best_iteration_)

avg_iter += model.best_iteration_

oof_preds[val_idx] = model.predict(X_val, num_iteration=model.best_iteration_)

sub['Target'] += model.predict(X_hold, num_iteration=model.best_iteration_)

fi = pd.DataFrame()

fi["feature"] = X_full.columns

fi["importance"] = model.feature_importances_

fi["fold"] = (i+1)

feature_importances = pd.concat([feature_importances, fi], axis=0)

print("Fold {} MAE: {:.8f}".format(i+1, mean_absolute_error(y_val, oof_preds[val_idx])))

print('In Sample MAE score %.8f' % mean_absolute_error(y_full, oof_preds))

print('Out of sample MAE: ', mean_absolute_error(y_hold, sub['Target']/n_splits))

print("avg iteration: ",(avg_iter/n_splits))

(110343, 29)

(88274, 29)

itteration: 100

Fold 1 MAE: 0.51615027

(110343, 29)

(88274, 29)

itteration: 100

Fold 2 MAE: 0.51819584

(110343, 29)

(88274, 29)

itteration: 100

Fold 3 MAE: 0.51731088

(110343, 29)

(88275, 29)

itteration: 100

Fold 4 MAE: 0.51331907

(110343, 29)

(88275, 29)

itteration: 100

Fold 5 MAE: 0.51443229

In Sample MAE score 0.51588171

Out of sample MAE: 0.5133541335204654

avg iteration: 100.0

## Naturally you expect this one to perform somewhat better and ineed it does

## No rediculous improvement, but improvement all the same.

Ensemble Submission

seed_dict

{1: 66, 5: 50, 9: 50, 12: 50, 20: 67}

random_seeds[4]

20

## Everything worked out exactely as I thought.

5

from sklearn.metrics import mean_absolute_error

sub = y_hold.to_frame()

sub["Target"] = 0

feature_importances = pd.DataFrame()

avg_iter = 0

ba= -1

for i, r in enumerate(range(n_splits)):

print(i)

ba = ba + 1

params["num_boost_round"] = int(seed_dict[random_seeds[ba]]*1.1)

params["seed"] = random_seeds[ba]

params["max_depth"] = depths[ba] # if you want to customise uncomment

model = LGBMRegressor(

**params

)

model.fit(

X_full,

y_full,

eval_metric='mae',

verbose=False

)

sub['Target'] += model.predict(X_hold)

fi = pd.DataFrame()

fi["feature"] = X_full.columns

fi["importance"] = model.feature_importances_

fi["fold"] = (i+1)

feature_importances = pd.concat([feature_importances, fi], axis=0)

print('Out of sample MAE: ', mean_absolute_error(y_hold, sub['Target']/n_splits))

0

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

1

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

2

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

3

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

4

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

Out of sample MAE: 0.5129196662064283

1.1 Out of sample MAE: 0.5129196662064283

from sklearn.metrics import mean_absolute_error

sub = y_hold.to_frame()

sub["Target"] = 0

feature_importances = pd.DataFrame()

avg_iter = 0

ba= -1

for i, r in enumerate(range(n_splits)):

print(i)

ba = ba + 1

params["num_boost_round"] = seed_dict[random_seeds[ba]]

params["seed"] = random_seeds[ba]

params["max_depth"] = depths[ba] # if you want to customise uncomment

model = LGBMRegressor(

**params

)

model.fit(

X_full,

y_full,

eval_metric='mae',

verbose=False

)

sub['Target'] += model.predict(X_hold)

fi = pd.DataFrame()

fi["feature"] = X_full.columns

fi["importance"] = model.feature_importances_

fi["fold"] = (i+1)

feature_importances = pd.concat([feature_importances, fi], axis=0)

print('Out of sample MAE: ', mean_absolute_error(y_hold, sub['Target']/n_splits))

0

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

1

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

2

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

3

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

4

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

Out of sample MAE: 0.5064183766351881

from sklearn.metrics import mean_absolute_error

mean_absolute_error(y_hold, y_pred)

# 0.5163493564074798

eval['l1-mean'][seed_best]

0.5155678000111037

from sklearn.model_selection import learning_curve

from lightgbm import LGBMRegressor

from sklearn.model_selection import ShuffleSplit

def plot_learning_curve(estimator, title, X, y, ylim=None, cv=None,

n_jobs=1, train_sizes=np.linspace(.1, 1.0, 5)):

"""

Generate a simple plot of the test and training learning curve.

Parameters

----------

estimator : object type that implements the "fit" and "predict" methods

An object of that type which is cloned for each validation.

title : string

Title for the chart.

X : array-like, shape (n_samples, n_features)

Training vector, where n_samples is the number of samples and

n_features is the number of features.

y : array-like, shape (n_samples) or (n_samples, n_features), optional

Target relative to X for classification or regression;

None for unsupervised learning.

ylim : tuple, shape (ymin, ymax), optional

Defines minimum and maximum yvalues plotted.

cv : int, cross-validation generator or an iterable, optional

Determines the cross-validation splitting strategy.

Possible inputs for cv are:

- None, to use the default 3-fold cross-validation,

- integer, to specify the number of folds.

- An object to be used as a cross-validation generator.

- An iterable yielding train/test splits.

For integer/None inputs, if ``y`` is binary or multiclass,

:class:`StratifiedKFold` used. If the estimator is not a classifier

or if ``y`` is neither binary nor multiclass, :class:`KFold` is used.

Refer :ref:`User Guide <cross_validation>` for the various

cross-validators that can be used here.

n_jobs : integer, optional

Number of jobs to run in parallel (default 1).

"""

plt.figure()

plt.title(title)

if ylim is not None:

plt.ylim(*ylim)

plt.xlabel("Training examples")

plt.ylabel("Score")

train_sizes, train_scores, test_scores = learning_curve(

estimator, X, y, cv=cv, n_jobs=n_jobs, train_sizes=train_sizes)

train_scores_mean = np.mean(train_scores, axis=1)

train_scores_std = np.std(train_scores, axis=1)

test_scores_mean = np.mean(test_scores, axis=1)

test_scores_std = np.std(test_scores, axis=1)

plt.grid()

plt.fill_between(train_sizes, train_scores_mean - train_scores_std,

train_scores_mean + train_scores_std, alpha=0.1,

color="r")

plt.fill_between(train_sizes, test_scores_mean - test_scores_std,

test_scores_mean + test_scores_std, alpha=0.1, color="g")

plt.plot(train_sizes, train_scores_mean, 'o-', color="r",

label="Training score")

plt.plot(train_sizes, test_scores_mean, 'o-', color="g",

label="Cross-validation score")

plt.legend(loc="best")

return plt

## There is no purpose for CV, I have enough data

params["num_boost_round"] = 72

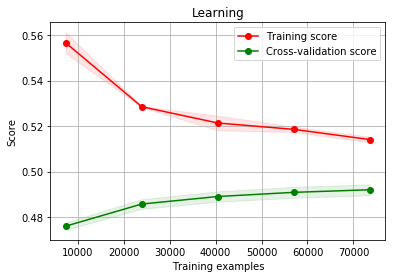

### They have converged enough, what this shows is that their is enough data in this task more data != higher score

plot_learning_curve(LGBMRegressor(**params), "Learning", df.drop(col_drop,axis=1), df["Satisfaction"], ylim=None, cv=None,

n_jobs=1, train_sizes=np.linspace(.1, 1.0, 5))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/lightgbm/engine.py:99: UserWarning: Found `num_boost_round` in params. Will use it instead of argument

warnings.warn("Found `{}` in params. Will use it instead of argument".format(alias))

<module 'matplotlib.pyplot' from '/Users/dereksnow/anaconda/envs/py36/lib/python3.6/site-packages/matplotlib/pyplot.py'>

tl;dr when the score is lower than it should be the bias is an issue it is underfitted, when the score is good for training but bad for validation curve then it is overfitting and has too much variance.

Firstly, we should focus on the right side of the plot, where there are sufficient data for evaluation.

If two curves are "close to each other" and both of them but have a low score. The model suffer from an under fitting problem (High Bias)

If training curve has a much better score but testing curve has a lower score, i.e., there are large gaps between two curves. Then the model suffer from an over fitting problem (High Variance)

All that has to happen is the cross validation score has to increase and eventually somewhat converge oveer time. If it doesn’t you are overfitting.

I think what you’re seeing is normal behaviour:

With only few samples (like 2000) it’s easy for a model to (over)fit the data - but it doesn’t generalize well. So you get high training accuracy, but the model might not work well with new data (i.e. low validation/test accuracy).

As you add more samples (like 9000) it becomes harder for the model to fit the data - so you get a lower training accuracy, but the model will work better with new data (i.e. validation/test accuracy starts to rise).

So:

As the training dataset increases, the training accuracy is supposed to decrease because more data is harder to fit well.

As the training dataset increases, the validation/test accuracy is supposed to increase as well since less overfitting means better generalization.

Andrew Ng has a video about learning curves. Note that he plots the error on the y axis, you have the accuracy on the y axis.. so the y axis is flipped.

Also take a look at the second half of the video. It explains high bias and high variance problems.

Your model seems to have high variance (due to the big “gap” between the two curves) - it’s still too complex for the small amount of data you’ve got. Either getting more data or using a simpler model (or more regularization on the same model) might improve the results.

#First of all, your training accuracy goes down quite a bit when you add more examples. So this could still be high variance. However, I doubt that this is the only explanation as the gap seems to be too big.

I understand that the gap between training and testing score is probably due to high variance(overfitting).

## Predicting, mean, median, mode, logistic and a groupby

Metrics

Bring in the holdoutset

y_pred = model.predict(X_hold)

from sklearn.metrics import mean_absolute_error

mean_absolute_error(y_hold, y_pred)

# 0.5163493564074798

0.5170065010722477

## Standard Benchmarks

y_mean = y_test.to_frame()

y_mean["Satisfaction"] = y_train.mean()

y_median = y_test.to_frame()

y_median["Satisfaction"] = y_train.median()

y_mode = y_test.to_frame()

y_mode["Satisfaction"] = y_train.mode().values[0]

print("Train")

print("Mean: ",mean_absolute_error(y_test, y_mean),

"Median: ",mean_absolute_error(y_test, y_median),

"Mode: ",mean_absolute_error(y_test, y_mode),

"Random",mean_absolute_error(y_test, y_train.sample(len(y_test))))

## Mean Test Distribution Peaking Naive Benchmark (TDPNB)

y_mean = y_test.to_frame()

y_mean["Satisfaction"] = y_test.mean()

# Median TDBPN

y_median = y_test.to_frame()

y_median["Satisfaction"] = y_test.median()

## Mode TDPNB

y_mode = y_test.to_frame()

y_mode["Satisfaction"] = y_test.mode().values[0]

print("Test Peaking")

print("Mean: ",mean_absolute_error(y_test, y_mean),

"Median: ",mean_absolute_error(y_test, y_median),

"Mode: ",mean_absolute_error(y_test, y_mode),

"Random",mean_absolute_error(y_test, y_test.sample(len(y_test))))

Train

Mean: 0.8252751318191531 Median: 0.8038245451265399 Mode: 0.8038245451265399 Random 1.0412092160197928

Test Peaking

Mean: 0.8248216444238886 Median: 0.8038245451265399 Mode: 0.8038245451265399 Random 1.0403587443946187

## This is going to give Laso some light.

def rmse_cv(model,X,y):

rmse = np.sqrt(-cross_val_score(model, X, y, scoring="neg_mean_squared_error", cv=5))

return rmse

def Standardisation(X_train, X_test, leave_out=None):

from sklearn.preprocessing import StandardScaler

if leave_out:

leave = X_train[leave_out]

X_train = X_train.drop(leave_out,axis=1)

listed = list(X_train)

scaler = StandardScaler()

try:

X_train = scaler.fit_transform(X_train)

except:

print("error_triggered")

X_train = scaler.fit_transform(X_train.fillna(X_train.mean()))

X_test = X_test.fillna(X_test.mean())

X_test = scaler.transform(X_test)

X_train = pd.DataFrame(X_train)

X_test = pd.DataFrame(X_test)

X_train.columns = listed

X_train = pd.concat((X_train,leave ),axis=1)

X_test.columns = listed

X_test = pd.concat((X_test,leave ),axis=1)

else:

scaler = StandardScaler()

listed = list(X_train)

try:

X_train = scaler.fit_transform(X_train)

except:

print("error_triggered")

X_train = scaler.fit_transform(X_train.fillna(X_train.mean()))

X_test = X_test.fillna(X_test.mean())

X_test = scaler.transform(X_test)

X_test = pd.DataFrame(X_test)

X_test.columns = listed

X_train = pd.DataFrame(X_train)

X_train.columns = listed

return X_train, X_test

X_train_s, X_test_s = Standardisation(X_train,X_test,[])

_, X_hold_s = Standardisation(X_train,X_hold,[])

error_triggered

error_triggered

## This is a quick and dirty way to do cs for lasso without plotting, but I want to plot the alphas, see below.

## Alpha is simply the regularisation term

model_lasso = LassoCV(alphas = [1, 0.1, 0.001, 0.0005]).fit(X_train_s, y_train)

Below we’ll run a ridge regression and see how score varies with different alphas. This will show how picking a different alpha score changes the R2.

Here, α (alpha) is the parameter which balances the amount of emphasis given to minimizing RSS vs minimizing sum of square of coefficients. α can take various values:

α = 0:

The objective becomes same as simple linear regression.

We’ll get the same coefficients as simple linear regression.

α = ∞:

The coefficients will be zero. Why? Because of infinite weightage on square of coefficients, anything less than zero will make the objective infinite.

0 < α < ∞:

The magnitude of α will decide the weightage given to different parts of objective.

The coefficients will be somewhere between 0 and ones for simple linear regression.

svr = SVR(gamma= 0.0004,kernel='rbf',C=13,epsilon=0.009)

#ker = KernelRidge(alpha=0.2 ,kernel='polynomial',degree=3 , coef0=0.8) ## too computationally expensive

ela = ElasticNet(alpha=0.005,l1_ratio=0.08,max_iter=10000)

bay = BayesianRidge()

## This is a great score without hyper-parametr tampering.

svr = ElasticNet(alpha=0.005,l1_ratio=0.08,max_iter=10000).fit(X_train_s, y_train)

y_svr = svr.predict(X_test_s)

mean_absolute_error(y_test, y_svr)

# 0.5006963184228322

0.5006963184228322

ela = SVR(gamma= 0.0004,kernel='rbf',C=13,epsilon=0.009).fit(X_train_s, y_train)

y_ela = ela.predict(X_test_s)

mean_absolute_error(y_test, y_ela)

bay = BayesianRidge().fit(X_train_s, y_train)

y_bay = bay.predict(X_test_s)

mean_absolute_error(y_test, y_bay)

score_kernel_ridge = []

alpha_space = np.logspace(-1, 0, 3)

for r in alpha_space:

kr = KernelRidge(alpha= r, kernel="polynomial", degree=3).fit(X_train_s, y_train)

y_kr = kr.predict(X_test_s)

score_kernel_ridge.append(mean_absolute_error(y_test, y_kr))

score_lasso = []

alpha_space = np.logspace(-10, 0, 20)

for r in alpha_space:

lasso = Lasso(alpha= r, normalize=True).fit(X_train_s, y_train)

y_lasso = lasso.predict(X_test_s)

score_lasso.append(mean_absolute_error(y_test, y_lasso))

score_lasso

score = []

alpha_space = np.logspace(-4, 0, 20)

for r in alpha_space:

ridge = Ridge(alpha= r, normalize=True).fit(X_train_s, y_train)

y_ridge = ridge.predict(X_test_s)

score.append(mean_absolute_error(y_test, y_ridge))

score

ridge_cv_scores = cross_val_score(ridge, X_scaled, y_train, cv=10)

ridge_cv_scores

score

score

Below we’ll run a ridge regression and see how score varies with different alphas. This will show how picking a different alpha score changes the R2. It is generally best not to run past the elbow.

from sklearn.linear_model import Ridge

# Create an array of alphas and lists to store scores

alpha_space = np.logspace(-20, 0, 10)

ridge_scores = []

ridge_scores_std = []

# Create a ridge regressor: ridge

ridge = Ridge(normalize=True)

# Compute scores over range of alphas

for alpha in alpha_space:

# Specify the alpha value to use: ridge.alpha

ridge.alpha = alpha

# Perform 10-fold CV: ridge_cv_scores

ridge_cv_scores = cross_val_score(ridge, X_scaled, y_train, cv=10)

# Append the mean of ridge_cv_scores to ridge_scores

ridge_scores.append(np.mean(ridge_cv_scores))

# Append the std of ridge_cv_scores to ridge_scores_std

ridge_scores_std.append(np.std(ridge_cv_scores))

# Use this function to create a plot

def display_plot(cv_scores, cv_scores_std):

fig = plt.figure()

ax = fig.add_subplot(1,1,1)

ax.plot(alpha_space, cv_scores)

std_error = cv_scores_std / np.sqrt(10)

ax.fill_between(alpha_space, cv_scores + std_error, cv_scores - std_error, alpha=0.2)

ax.set_ylabel('CV Score +/- Std Error')

ax.set_xlabel('Alpha')

ax.axhline(np.max(cv_scores), linestyle='--', color='.5')

ax.set_xlim([alpha_space[0], alpha_space[-1]])

ax.set_xscale('log')

plt.show()

# Display the plot

display_plot(ridge_scores, ridge_scores_std)

import matplotlib

coef = pd.Series(model_lasso.coef_, index = X_train.columns)

print("Lasso picked " + str(sum(coef != 0)) + " variables and eliminated the other " + str(sum(coef == 0)) + " variables")

imp_coef = pd.concat([coef.sort_values().head(10),

coef.sort_values().tail(10)])

matplotlib.rcParams['figure.figsize'] = (8.0, 10.0)

imp_coef.plot(kind = "barh")

plt.title("Coefficients in the Lasso Model")

df.shape

## Scaled Data

## PCA Data

pca = PCA(n_components=410)

X_scaled=pca.fit_transform(X_scaled)

def rmse_cv(model,X,y):

rmse = np.sqrt(-cross_val_score(model, X, y, scoring="neg_mean_squared_error", cv=5))

return rmse

def Standardisation(df, leave_out=None):

from sklearn.preprocessing import StandardScaler

if leave_out:

leave = df[leave_out]

df = df.drop(leave_out,axis=1)

listed = list(df)

scaler = StandardScaler()

try:

scaled = scaler.fit_transform(df)

except:

print("error_triggered")

scaled = scaler.fit_transform(df.fillna(df.mean()))

df = pd.DataFrame(scaled)

df.columns = listed

df = pd.concat((df,leave ),axis=1)

else:

scaler = StandardScaler()

listed = list(df)

try:

scaled = scaler.fit_transform(df)

except:

print("error_triggered")

scaled = scaler.fit_transform(df.fillna(df.mean()))

df = pd.DataFrame(scaled)

df.columns = listed

return df

X_scaled = Standardisation(X_train,[])

X_scaled.shape

y_train.shape

## Machine Learning Benchmarks

## In linear models a PCA step can work nicely

from sklearn.model_selection import cross_val_score, GridSearchCV, KFold

from sklearn.linear_model import LinearRegression

from sklearn.linear_model import Ridge

from sklearn.linear_model import Lasso

from sklearn.ensemble import RandomForestRegressor, GradientBoostingRegressor, ExtraTreesRegressor

from sklearn.svm import SVR, LinearSVR

from sklearn.linear_model import ElasticNet, SGDRegressor, BayesianRidge

from sklearn.kernel_ridge import KernelRidge

from xgboost import XGBRegressor

models = [LinearRegression(),Ridge(),Lasso(alpha=0.01,max_iter=10000),RandomForestRegressor(),GradientBoostingRegressor(),SVR(),LinearSVR(),

ElasticNet(alpha=0.001,max_iter=10000),SGDRegressor(max_iter=1000,tol=1e-3),BayesianRidge(),KernelRidge(alpha=0.6, kernel='polynomial', degree=2, coef0=2.5),

ExtraTreesRegressor(),XGBRegressor()]

names = ["LR", "Ridge", "Lasso", "RF", "GBR", "SVR", "LinSVR", "Ela","SGD","Bay","Ker","Extra","Xgb"]

for name, model in zip(names, models):

score = rmse_cv(model, X_scaled, y_train.reset_index(drop=True))

print("{}: {:.6f}, {:.4f}".format(name,score.mean(),score.std()))

1+1

lasso=Lasso(alpha=0.001)

lasso.fit(X_scaled,y_log)

y_pred = model.predict(X_test)

from sklearn.metrics import mean_absolute_error

mean_absolute_error(y_test, y_pred)

p_testa

## It has been a long time sinced I used learning curves, and I think it is worth adding one again, and saying something about how much data is needed

Learning Curves: If you plot cross-validation (cv) error and training set error rates versus training set size, you can learn a lot. If the two curves approach each other with low error rate, then you are doing well.

If it looks like the curves are starting to approach each other and both heading/staying low, then you need more data.

If the cv curve remains high, but the training set curve remains low, then you have a high-variance situation. You can either get more data, or use regularization to improve generalization.